There’s been quite a bit of talk recently about the upcoming AIB IPO and no doubt many people will be considering investing some of their hard earned cash in the bank although I have to say it baffles me why this is the case.

I think that most people will accept that the ordinary Joe Bloggs who buys shares does so based on a whim rather than any knowledge of the underlying investment. There is no fundamental analysis of the financials of the company, no assessment of the management team and no concept of any of the tools of investment theory that might assist in making an informed decision on whether the investment is likely to perform. Banks themselves refer to this type of investing as speculation and for that reason they don’t lend to fund it it unless there is a secondary source of repayment (other money which can repay the loan if the investment doesn’t perform) and the security pledged is very valuable. Professional fund managers spend a huge amount of time and money assessing and selecting undervalued stocks, identifying factors which might indicate future performance, devising ways of investing which reduce risk and/or enhance return and despite this, even they get it wrong.

Even though non-professional investors know full well that they could lose a substantial amount of money, this doesn’t scare people off. The chance of making easy money without breaking a sweat is too attractive.

Firstly, there’s plenty I could say about the underlying business to bolster a case for not investing in it, like the fact that when you hear about disruption in banking it invariably is referring to IT systems going down i.e. bad disruption. Banking is ripe for a different type of disruption, that is disruptive innovation but it isn’t happening. There isn’t a Chief Executive of a bank alive who has any real ideas about how to disrupt banking in a way that will help the bank he runs to stand out from the competition. To quote Mike Myatt “without a disruptive focus you are merely building your business model on a me too platform of mediocrityâ€. You can invest in any bank stock so if you decide to invest in AIB surely it should be because you’ve identified that it has something going for it that it’s competitors don’t.

In this post I am going to show you one of the tools used by professional fund managers to reduce risk. You can’t do this yourself but it might cause you to question whether investing directly in shares (in any company) is a good idea.

Many non-professional investors who invest in AIB will only own shares in one company or at best in a very small number of companies. I’m not going to waste space outlining the benefits of diversification because you’ve likely heard all about that and if you are still considering investing in AIB and probably owning just it and little or nothing else, you obviously don’t care about diversification.

I’m going to assume however that you are a rational investor (or at least a rational person) so when investing your money you want to obtain the highest expected return with the lowest exposure to risk. This is an assumption which is used when considering investment theory as logically it has to be the case.

The key to what I am going to outline is based on concept called correlation. This gets just a bit technical but if you’re thinking of pouring your children’s inheritance into the stock market it’s worth reading.

Correlation is the extent to which the price of a share moves in unison with the price of a second share.

- If two shares move the same amount in the same direction they are said to have a correlation coefficient of 1, or they are said to be perfectly correlated.

- If they move the same amount in opposite directions then the two shares are said to have a correlation coefficient of -1, or they are said to be perfectly uncorrelated (this is the ideal but it doesn’t happen in real life).

- What you can get is a low positive correlation of somewhere between +0.2 and +0.6.

When two shares with a low positive correlation are combined in a portfolio, there is a reduction in risk versus the risk level which would pertain if only one of the shares was invested in. This occurs because worse than expected returns from one share are offset by better than expected returns from the other share. By combining the two shares some of their fluctuations cancel each other out.

Combining stocks doesn’t affect expected return. The expected return is still the weighted return of the stocks.

However the standard deviation (risk) is not the weighted standard deviations of the two shares – it is calculated using a formula which includes the correlation number and if that number is low and positive, then the standard deviation will be less than the weighted standard deviation of the two shares. This is important as it allows you to combine shares to achieve less risk than would exist if each of the constituent stocks were invested in on their own. I realise that this is getting heavy and not everyone cares for the maths involved – if you want to skip the numbers just scroll down a few inches to Why does the above matter?

Taking two shares with a correlation coefficient of 0.2 and the following Expected Returns and Risk;

| Expected Return | Risk | |

| Share A | 10% | 15% |

| Share B | 20% | 25% |

If you calculate the various combinations of investment you get the following Expected Returns and Risk;

| Proportion invested | Proportion invested | Portfolio | Portfolio |

| in Share A | in Share B | Expected Return | Risk |

| 100% | 0% | 10% | 15% |

| 80% | 20% | 12% | 14% |

| 60% | 40% | 14% | 15% |

| 40% | 60% | 16% | 17% |

| 20% | 80% | 18% | 21% |

| 0% | 100% | 20% | 25% |

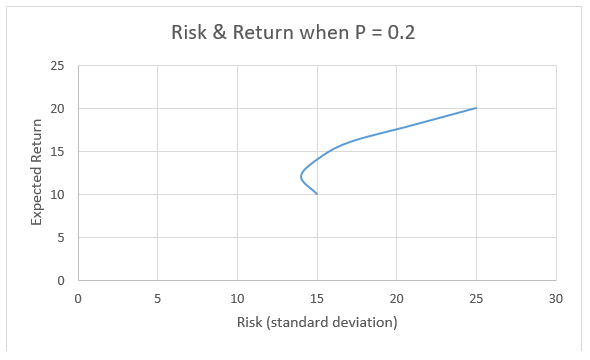

If you then plot this on a chart of Risk and Expected Return it looks like this;

The lower end point of the blue line represents portfolio Risk and Expected Return if you invest 100% in share A and nothing in share B. The top point represents no investment in share A and 100% in share B. In between are mixes of investment in share A and share B (80:20, 60:40 etc).

As you can see from the table above there are two combinations of investment which result in a Risk level of 15%, all of the fund invested in Share A or alternatively by having only 60% of it in Share A and the remaining 40% of your money in Share B. Having all of your investment in Share A will give you an Expected Return of 10%. Having 60% in A and 40% in B however will give you an Expected Return of 14%, for the same level of Risk (15%). Obviously any investor would choose to have an Expected Return of 14% rather than 10% for a given level of Risk.

Why does the above matter

The graph shows that investing only in share A is nonsensical as investing in a combination of A and B gives you the same Risk level but a higher Expected Return. Remembering that you are a rational investor you cannot possibly choose the lower expected return with the same level of risk that you get by investing in one share as this would be illogical in the context of wanting to maximise return and minimise risk. You therefore cannot logically choose to invest in a single share if you could get a higher return with the same level of risk by investing in two shares which have a low correlation.

WARNING: DO NOT TRY THIS AT HOME

I’m not suggesting for a moment that you go out and buy shares in two companies instead of one. There are a number of reasons why this isn’t the solution;

- The above is only a simple demonstration of this concept; actually putting it in practice is best left to professional fund managers

- The reduction in risk from adding one additional share to your portfolio may not be sufficient to offset the transaction costs involved, especially for smaller portfolios

- Stock selection is all important, especially when you are investing in a relatively small number of stocks. If you invest in the wrong stocks low correlation won’t save you

- In the short term equities are too risky an investment for anyone. You need to find ways of reducing the volatility (risk) of your investment. Professional fund managers construct portfolios which are designed to do this

- The theory demonstrated above holds as you increase the number of shares in your portfolio, in fact as you increase the number of shares involved the risk level of the individual shares becomes less important and the extent to which they are correlated becomes more important. What happens when you add more lowly correlated shares to your portfolio is that you push the line on the graph above, to the left and up which means that you get a higher Expected Return with a lower level of Risk. To achieve this in a meaningful way would incur significant transaction costs which would only be viable for larger portfolios. As the transaction costs involved would not be justified for smaller portfolios this can only be done by professional fund managers working with large portfolios

Direct investment in shares is not suitable for the vast majority of people. There are a wide variety of investment funds available in the market which use the above and other strategies to reduce risk and maximise return at less cost than you could ever do it. Whilst their success varies, they rarely fail like a bad investment in a single share does.

If you have an investment need and are interested in exploring your options, contact Eoghan on 086 606 5008, by using the contact form below, or by email to eoghan@obn.ie.

Comments in this blog are general in nature and should not be taken as financial advice as no assessment has been undertaken in relation to your financial situation or objectives.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in this product you may lose some or all of the money you invest

© Eoghan Gavigan 12 June 2017

Contact OBN